The Survey on the Access to Finance of Enterprises: monetary policy, economic and financing conditions and inflation expectations

Published as part of the ECB Economic Bulletin, Issue 7/2024.

1 Introduction

The Survey on the Access to Finance of Enterprises (SAFE) provides a comprehensive overview of the economic and financing conditions of firms across the euro area.[1] The SAFE, launched in 2009, is a euro area survey conducted jointly by the European Central Bank (ECB) and the European Commission. It gives crucial insight into the financing conditions of firms, their economic performance, and, more recently, their expectations with regard to selling prices, wages, number of employees and overall consumer price inflation in the euro area. The survey provides the ECB with highly informative data that feeds directly into the monetary policy decision-making process.

The survey provides extensive and useful coverage of euro area enterprises, with a particular focus on small and medium-sized enterprises (SMEs). In spite of the significant role played by SMEs in driving economic growth and employment, data on the financing decisions of SMEs have tended to be rather scarce. Given that SMEs depend chiefly on bank financing, this survey provides important information on the bank-based transmission of monetary policy.

Analyses based on SAFE data have consistently demonstrated that monetary policy affects firms’ perceptions of current financing conditions, as well as their expectations of the future availability of external financing. These perceptions and expectations are critical given that they influence the real economic performance of firms, as reflected in their investment and employment decisions, and in overall GDP growth in the euro area.

New quantitative questions on the pricing and cost expectations of firms now provide additional information, enhancing the importance of the survey in policymaking. This survey therefore enriches existing ECB surveys on the inflation expectations of households, economists and market participants with its data on the consumer price inflation expectations of firms, as well as with its questions on firms’ expected selling prices and wages.[2]

In 2024 the frequency of survey rounds was increased from twice yearly to quarterly in response to the need for more timely data. This has enabled more recent data to be captured, which is of particular importance during periods of economic turbulence and rapid policy shifts, as well as the inclusion of ad hoc questions on highly relevant topics, such as the impact of climate change or factors influencing changes in the average hours worked.[3]

This article is structured as follows. Section 2 illustrates how monetary policy affects firms’ access to finance, followed by a box examining the co-movements of SAFE-based indicators and financial market indices. Section 3 focuses on the impact of economic crises on the performance of firms, with Section 4 exploring future GDP developments. Finally, Section 5 presents the new modules on firms’ expectations for selling prices, wages and inflation.

2 Evidence of transmission of monetary policy to firms’ access to finance

The price- and quantity-based financing indicators derived from the survey data help measure monetary policy effects on firms’ financing conditions. These indicators specify the changes perceived by firms in the pricing and terms and conditions of financing, including bank interest rates and other costs of bank financing such as charges, fees and commissions. Firms also report perceived changes in terms of the supply of and demand for bank loans, as well as the financing gap between supply and demand.[4] The expectations of firms regarding future changes in the availability of bank loans in the coming six months, as well as the availability of other sources of external financing, are also included in the survey’s questionnaire.

Survey-based indicators of financing conditions at firm level provide insight into the “downstream” stages of monetary policy transmission. At the initial “upstream” stages of this mechanism, there is the pass-through of the ECB’s key policy interest rates to risk-free interest rates and sovereign yields. Changes in market funding costs[5] influence, either directly or indirectly (e.g. via banks), firms’ “downstream” funding costs and volumes, including financing gaps. Box 1 shows that financial market variables strongly co-move with the financing gap and contribute to its dynamics over time.

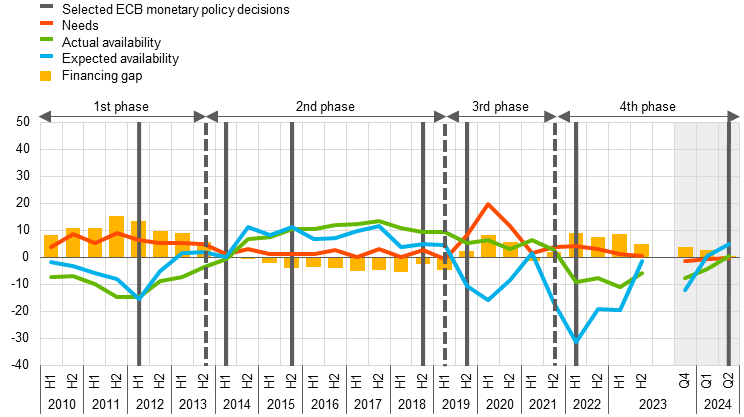

From 2010 to date, survey data show that firms’ perceptions of their financing conditions can be broken down into four key phases (Charts 1 and 2). These phases broadly reflect the ECB’s monetary policy decisions over that time.[6] The first phase, from the launch of the survey until the first quarter of 2014, consisted of the introduction of several non-standard policy measures and the announcement of the Outright Monetary Transactions programme. The second phase, from the second quarter of 2014 to shortly before the outbreak of the COVID-19 pandemic, was when the ECB expanded its toolkit to ease financing conditions. The third phase began with the outbreak of the pandemic and ended before the first ECB policy rate increase in July 2022.The last phase was marked by multiple ECB interest rate increases in response to a sharp surge in inflation and expectations of sustained high inflation.

During the first phase, a high but declining net percentage of firms reported rising interest rates (Chart 1) and positive financing gaps (Chart 2). The sovereign debt crisis primarily negatively affected bank loan availability, given that banks faced difficulties obtaining liquidity from the wholesale market, resulting in diverging lending conditions across euro area countries. To address these challenges, the ECB introduced various non-standard monetary policy measures and cut its interest rates. The “whatever it takes” speech by former President Mario Draghi at the end of July 2012, and the subsequent announcement of the Outright Monetary Transactions programme, marked a turning point for the euro area, leading to an immediate contraction in sovereign bond spreads to more sustainable levels. This decline mitigated banking sector funding problems, restored bank lending dynamics and improved overall financing conditions. By the end of this phase, in net terms, firms reported declining interest rates and positive, but lower, financing gaps, indicating improved access to bank loans (i.e. the supply of loans exceeded the demand for loans).

Chart 1

Changes in bank loan pricing and terms and conditions

a) Small and medium-sized enterprises

(net percentages)

b) Large firms

(net percentages)

Source: Survey on the Access to Finance of Enterprises.

Notes: The figures are based on firms that applied for bank loans (including subsidised bank loans), credit lines, or bank or credit card overdrafts. Respondents who replied “not applicable” or “don’t know” have been excluded. Net percentages are the difference between the percentage of firms that reported an increase for a given factor and the percentage that reported a decrease. On the x-axis, H1 stands for the reference period from the second to the third quarter and H2 for the reference period from the fourth quarter to the first quarter of the following year. The grey-shaded segments of the charts reflect responses to the same question but on a quarterly basis. The dotted vertical lines indicate different phases of financing conditions. The first phase begins with the launch of the survey and ends in the first quarter of 2014; the second phase spans from the second quarter of 2014 to shortly before the outbreak of the COVID-19 pandemic; the third phase begins with the outbreak of the pandemic and ends in the first quarter of 2022 and the last phase starts in the second quarter of 2022. The first vertical grey line denotes the announcement of the Outright Monetary Transactions programme in September 2012; the second, the start of the first series of targeted longer-term refinancing operations (TLTRO I) and the negative interest rate policy; the third, the start of TLTRO II and the corporate sector purchase programme; the fourth, the announcement of TLTRO III; the fifth, the start of the pandemic emergency purchase programme in March 2020; the sixth, the rise of the three key ECB interest rates by 50 basis points and the approval of the Transmission Protection Instrument; the last, the cut in the three key ECB interest rates by 25 basis points in June 2024. The latest observations are for the period from October 2023 to March 2024 for the biannual series and for the second quarter of 2024 for the quarterly series.

Chart 2

Changes in needs, actual and expected bank loan availability and the financing gap

a) Small and medium-sized enterprises

(net percentages)

b) Large firms

(net percentages)

Source: Survey on the Access to Finance of Enterprises.

Note: See the Notes to Chart 1.

In the second phase, from April 2014 to shortly before the outbreak of the COVID-19 pandemic, favourable financing conditions prevailed, even though SME financing conditions had not improved as much as for large firms. During this period, the ECB expanded its monetary policy toolkit to ease financing conditions and enhance the transmission of its accommodative monetary policy stance.[7] Notwithstanding the overall loosening of financing conditions, as reflected in the negative financing gaps, fewer SMEs than large firms reported declining interest rates. This highlights the different risk assessments that banks applied to various firm size classes.

The third phase, from the outbreak of the pandemic until March 2022, was marked by high economic and geopolitical uncertainty, with firms signalling greater demand for external financing. At the peak of the pandemic, firms reported a noticeable spike in the demand for bank loans. Although the ECB and euro area governments intervened swiftly, there was a time lag before these actions could take effect and ultimately ease the liquidity constraints that firms faced as a result of lockdown measures.[8] Firms reported that access to bank loans had increased, but this did not prevent an increase in financing gaps. After the outbreak of the pandemic, SMEs reported declining interest rates, while large firms fairly soon began to report signs of increases. This disparity likely reflects the fact that most of the public intervention schemes announced during the early stages of the pandemic were targeted at SMEs. Overall, by the end of the third quarter of 2021 (H1 2021 in Charts 1 and 2), financing conditions had begun to improve. However, this phase ended with a slowdown in economic activity, amid heightened geopolitical uncertainty linked to the war in Ukraine, and a widespread reassessment of risk perceptions by banks. These factors led to tighter lending conditions in terms of interest rates and a fall in credit supply already in early 2022, before the first policy rate hike by the ECB in July 2022.

The fourth phase, starting in April 2022, saw high financing gaps and the largest recorded net share of firms to have reported increases in interest rates since the survey began. Already in the first quarter of 2022, hence prior to the ECB’s initial interest rate hike in July 2022, 6% of euro area banks tightened their credit standards, as indicated in the ECB’s euro area bank lending survey on loans to non-financial corporations. This percentage rose further in anticipation of the initial step in the ECB’s tightening cycle, which was in the third quarter. By the end of 2022, the percentage of banks that tightened their credit standards had climbed to 27% and it remained at that level in the first quarter of 2023.[9] At the same time, most firms, irrespective of their size, reported in the SAFE net increases in interest rates, with the highest net percentage ever to be recorded since the survey began. The reported financing gap widened and was mainly driven by a decline in the availability of external financing, reflecting the broad-based pass-through of monetary policy tightening.

The new quarterly survey data indicate that since the last quarter of 2023 firms have reported slight improvements in financing conditions, albeit the conditions remaining tight.[10] This is the period when the tightening of the monetary policy stance came to an end and expectations of an easing gradually emerged. Between the last quarter of 2023 and the second quarter of 2024, the net percentage of firms that reported increases in interest rates nearly halved. At the same time, the financing gap narrowed, falling to zero for SMEs and turning from positive to slightly negative for large firms. This was primarily on account of the increased availability of bank loans across firm size classes, which was more pronounced for large firms.

The expectations by firms of future credit availability play an important role in the “bank lending channel” of monetary policy.[11] Firms are also asked about their expectations concerning the availability of credit over the next six months. As illustrated in Chart 2, changes in expected bank loan availability are a reliable indicator of the shifts in actual access to external financing in subsequent periods.

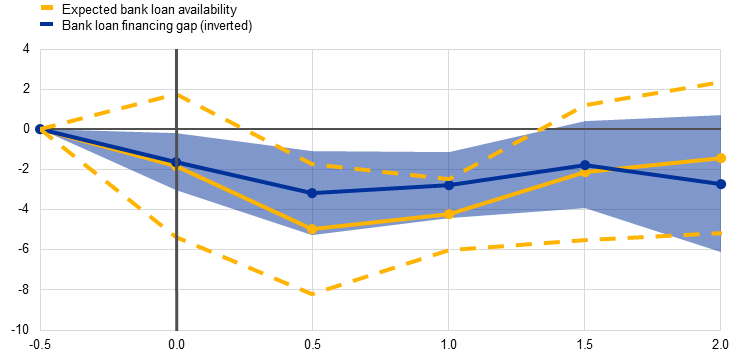

Monetary policy decisions greatly influence expectations of future credit supply and financing gaps. A tightening of monetary policy lowers firms’ expectations of the availability of future bank loans, which in turn affects their real decisions, even before any actual change in credit conditions occurs.[12] Moreover, it is seen to widen firms’ financing gaps and lower their expectations about future bank loan availability (Chart 3).[13] These effects can persist up to two years following a shock, demonstrating the significant impact of monetary policy on firms’ financing conditions via the credit supply channel. In addition, other empirical analyses show that firms closely monitor the ECB’s monetary policy when policy announcements are made but react to them differently depending on their news content.[14] When the news content is moderate or perceived as positive for the availability of bank loans, firms react less quickly and are less concerned. However, when the announcements involve significant shocks and convey negative news regarding credit availability, firms respond swiftly by adjusting their bank loan expectations.

Chart 3

Response of financing gaps and expectations of future bank loan availability to a monetary policy shock

(x-axis: years after shock; y-axis: percentage point changes compared with period before shock)

Source: Box entitled “Firms’ access to finance and the business cycle: evidence from the SAFE”, Economic Bulletin, Issue 8, ECB, 2022.

Notes: Response of firms’ financing gaps and the net percentage of firms that reported an expected increase in the availability of bank loans over the next six months after a one-standard deviation monetary policy shock. The shock used in the regression analysis is the target factor from Altavilla, C. et al., “Measuring euro area monetary policy”, Journal of Monetary Economics, Vol. 108, Elsevier, 2019, pp.162-179. The shock captures monetary policy surprises at the very short end of the Overnight Index Swap curve in and around ECB monetary policy announcements. The effect of the monetary policy shocks on the SAFE variables are estimated using local projection methods. The shaded area and the dashed lines denote the 95% confidence intervals. The latest observations are for the period from April to September 2021.

Box 1

Linking financial market data and SAFE-based indicators of firms’ financing gaps

This box examines how some key financial market variables contribute to financing gap dynamics over time.

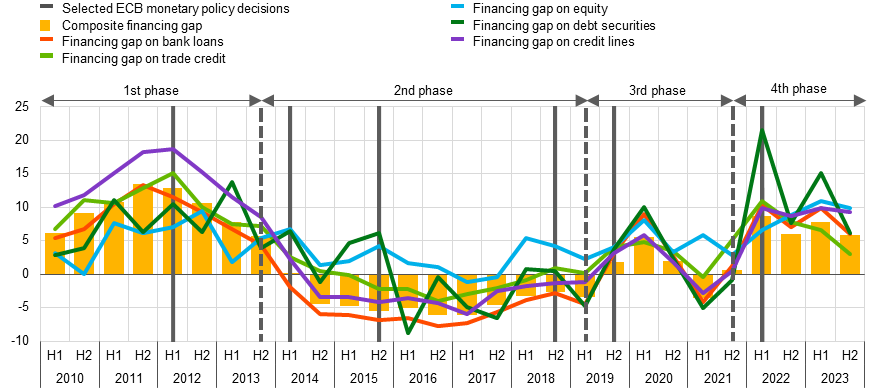

The survey provides information on changes in firms’ financing gaps across various sources of external financing, such as bank loans, credit lines, trade credit, as well as equity and debt securities issuance. The composite financing gap indicator is constructed as a weighted average of the financing gaps for each individual instrument. While the composite financing gap appears to closely co-move with the financing gap for bank loans (Chart A), the discrepancy between the two measures suggests that firms may rely on various sources of external financing to support their activities.[15]

Chart A

Composite financing gap of firms and its components

(net percentages)

Source: Survey on the Access to Finance of Enterprises.

Notes: The financing gap indicators combine both financing needs and the availability of bank loans, trade credit, equity, securities and credit lines at firm level. For each of the five financing instruments, the indicator of the perceived change in the financing gap takes a value of 1 (-1) if the need increases (decreases) and the availability decreases (increases). If enterprises perceive only a one-sided increase (decrease) in the financing gap, the variable is assigned a value of 0.5 (-0.5). The composite financing gap is computed at firm level by adding together the financing gaps for each relevant source of financing and then dividing this total by the number of these sources. A positive value for the indicator points to an increase in the financing gap. Values are multiplied by 100 to obtain weighted net balances in percentages. See also the Notes to Chart 1. The latest observations are for the period from October 2023 to March 2024.

Chart B

Firms’ composite financing gap and selected financial market variables

(left-hand scale: standard deviation; right-hand scale: net percentages)

Sources: Survey on the Access to Finance of Enterprises, Refinitiv Datastream, Bloomberg, iBoxx, ECB calculations.

Notes: The excess cyclically adjusted price-to-earnings ratio (CAPE) yield is the real excess return on European stocks relative to government bonds, the OIS1Y is the one-year Overnight Index Swap (OIS) rate, the Brent oil price is the cost per barrel of Brent crude oil, the Volatility Index (VIX) is the index that measures market expectations of future volatility based on the price of options on the S&P 500 Index, the government bond spread (IT-DE 10Y) is the difference between Italian and German 10-year bond yields. The financial market variables have daily frequencies and are shown in terms of deviations from their long-term averages. Values for the composite financing gap are those from the biannual series. For the financing gap, see the Notes to Chart A, for net percentages and for the various ECB monetary policy decisions, see the Notes to Chart 1. The latest observations are for the period from October 2023 to March 2024 for the survey and for 22 July 2024 for the financial data.

To assess the relationship between the daily financial market variables in Chart B and the composite financing gap in the SAFE, a linear model is applied to the biannual data from the SAFE. An analysis of the estimated contributions of these variables over time provides insight into the factors that could influence changes in the composite financing gap (Chart C). Examining the four key phases of perceived financing conditions outlined in Section 2 indicates that the increase in the composite financing gap during the first phase correlates with rising oil prices and higher risk premia. In the second phase, lower uncertainty, falling oil prices and negative risk-free rates were primarily associated with a decrease in the financing gap. The third phase saw a large increase in the financing gap at the onset of the pandemic. The model attributes this change to the positive contribution of greater uncertainty. In the fourth phase, the composite financing gap reached its highest net percentage level since the sovereign debt crisis. The model ascribes the increase seen over the summer of 2022 (H1 2022 in Chart C) primarily to rising oil prices and heightened uncertainty (proxied by the Volatility Index - VIX). Thereafter, high risk-free rates were the main driver of changes in the financing gap, which shows that the ongoing transmission of monetary policy tightening had reached its “downstream” stages.

Chart C

Contribution of financial market variables to changes in composite financing gap

(net percentages)

Sources: Refinitiv Datastream, Bloomberg, iBoxx, Survey on Access to Finance of Enterprises, ECB calculations.

Notes: CAPE stands for cyclically adjusted price-to-earnings ratio, OIS IY for the one-year Overnight Index Swap rate and VIX for the Volatility Index. The chart plots the contribution of each financial market variable to the composite financing gap at each point in time. The contributions are computed using the coefficient of the regression of the composite financing gap on the financial market variables described in Chart B. The constant is omitted. The residual is the difference between the actual value of the composite financing gap and the value predicted by the model. For a description of the financial market variables, see the Notes to Chart B. The latest observations are for the period from October 2023 to March 2024. The financial market variables are aggregated to biannual frequency using averages over the same six-month periods as those of the SAFE sample.

3 Impact of economic and financial crises on firm performance

Understanding the heterogeneous effects of economic and financial crises on firms of different sizes is important for crafting effective policy responses. The impact of economic and financial crises can vary significantly between SMEs and large firms, influencing their ability to sustain operations, manage costs and recover. The SAFE provides valuable data for a granular and timely assessment of these differential effects.

The sovereign debt crisis saw a significant decline in firms' turnover and profits, while both labour and non-labour costs remained stable (Chart 4). During this period – from the third quarter of 2011 to the first quarter of 2013 – the crisis drastically disrupted financial markets and real economic activity in the euro area. SMEs experienced a rapid decline in turnover from the onset of the crisis (Chart 4), while for large firms the economic repercussions were less severe. Throughout the crisis, the share of firms that reported higher labour, material and energy costs remained relatively stable across the two size classes. Profits declined significantly, with SMEs being the most affected by the adverse economic environment.

Chart 4

Changes in the economic situation of euro area firms

a) Small and medium-sized enterprises

(net percentages)

b) Large firms

(net percentages)

Source: Survey on the Access to Finance of Enterprises.

Notes: See the Notes to Chart 1. The latest observations are for the period from October 2023 to March 2024 for the biannual series and for the second quarter of 2024 for the quarterly series.

The outbreak of the pandemic and the subsequent economic recession had a similar negative impact on SMEs and large euro area firms, but large firms were quicker to recover (Chart 4). In spite of widespread state aid measures, firms experienced sharp declines in their turnover and profits.[16] In the first half of 2020 (H1 2020 in Chart 4), the net percentage of firms to have reported an increase in labour, raw material and energy costs also plummeted for SMEs and large firms alike, largely reflecting a fall in production-related activities. Thanks to various government guarantees for bank loans, only around 5% of firms reported an increase in interest expenses, which was similar across firm sizes. However, while large firms’ economic activity stabilised between the fourth quarter of 2020 and the first quarter of 2021 (H2 2020 in Chart 4), SMEs lagged behind, still reporting a significant decrease in turnover.

In contrast to the pandemic crisis, the energy price crisis saw unprecedented increases in non-labour and labour costs, just as firms were starting to recover (Chart 4). From the second quarter of 2021, turnover broadly increased as the economy rebounded. However, euro area firms struggled to keep pace with rising input costs. Material and energy costs surged, with almost all firms reporting increases between the second and third quarter of 2022 (H1 2022 in Chart 4). Labour costs also rose considerably, as reported by a record 73% of SMEs and 84% of large firms.

Although a higher net percentage of large firms reported increases in input costs compared with SMEs, the significant rise in turnover in mid-2022 enabled large firms to offset somewhat the growing pressure on their profit margins. By contrast, SMEs reported four consecutive semesters of net decreases in profits, with the highest share of firms reporting net decreases between the second and third quarter of 2022 (H1 2022 in Chart 4).

Immediately after the energy price crisis, firms faced the steepest increase in interest expenses ever to be recorded by this survey. Following the rise in inflation and the subsequent tightening of monetary policy, the survey responses indicated that a record 58% of large firms and 40% of SMEs had experienced a rise in interest expenses.

4 Leading indicator properties for euro area activity

The composite financing gap and expectations of the availability of external financing are correlated with current and future real GDP growth in the euro area (Chart 5). An increase in euro area activities (i.e. positive real GDP growth) has usually moved in parallel with declining composite financing gaps, as well as greater optimism about the future availability of external financing. As in previous studies, it is possible to estimate average euro area real GDP growth developments following changes in the composite financing gap and in the expected availability of external financing.[17] While these estimates do not establish causal effects, they do provide an indication of average future developments in real GDP growth following a change in the SAFE indicators of the aforementioned variables.

Chart 5

Composite financing gap of firms, expected external financing availability and euro area real GDP growth

(net percentage changes in the composite financing gap and in the expected availability of external financing; annualised percentage changes in GDP growth)

Sources: Survey on the Access to Finance of Enterprises and Eurostat.

Notes: For the composite financing gap, see the Notes to Chart A in Box 1. The indicator of the expected availability of external financing is a weighted sum of the availability of each of the five financing instruments considered in the composite financing gap. For the net percentages and the different ECB monetary policy decisions, see the Notes to Chart 1. The latest observations are for the period from October 2023 to March 2024 for the survey and for March 2024 for real GDP growth.

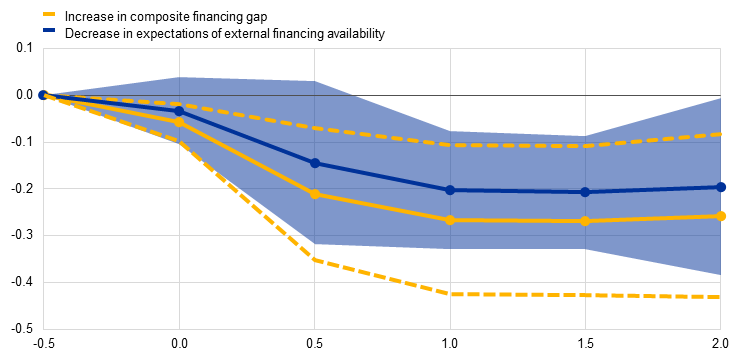

Following a 1 percentage point increase in the composite financing gap, real GDP in the euro area declines, on average, by 0.3% over the subsequent year (Chart 6). This decline is constant over the next 18 months but becomes less significant after two years. Conversely, following a decrease of 1 percentage point in the expected availability of external financing, real GDP in the euro area declines, on average, by approximately 0.2% over the subsequent year. These estimates are conditional on lagged real GDP growth, thus exploiting the information from the survey beyond past observable developments in the business cycle.

Chart 6

Average developments in euro area real GDP growth following a deterioration in financing conditions as compared with no deterioration

(x-axis: years after shock; y-axis: cumulative growth in percentages relative to period before the shock)

Sources: Survey on the Access to Finance of Enterprises and ECB calculations.

Notes: Average developments in euro area real GDP growth in cumulative terms following changes in firms’ financing gaps and the net percentage of firms that reported an expected increase in the availability of external financing (bank loans, credit lines, trade credit, equities and debt securities). The regression analysis uses local projections and includes current and past GDP growth as control variables. The shaded area and the dashed lines denote 95% confidence bands. The latest observations are for the period from October 2023 to March 2024 for the survey and for March 2024 for real GDP growth.

5 Price and inflation expectations

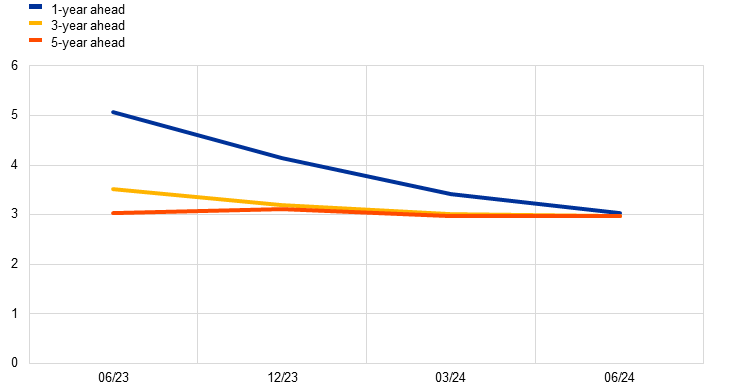

Since the second quarter of 2023, the SAFE has been supplemented with data on euro area firms’ inflation expectations, thus addressing a significant information gap. The inflation expectations of euro area firms have so far not been measured in a consistent manner across countries. The 2020/21 ECB monetary policy strategy review brought this information gap to light.[18] From the first quarter of 2024, euro area inflation expectations for the one-year, three-year and five-year horizons, together with firms perceived uncertainty surrounding their five-year inflation expectations, have been available on a quarterly basis.[19]

Firms’ median inflation expectations have steadily declined since the second quarter of 2023 at the one-year horizon. Euro area firms’ one-year ahead median inflation expectations fell to 3% in June 2024 from a peak of 5% in June 2023, in line with disinflationary developments (Chart 7, panel a). SMEs have significantly higher inflation expectations than large firms, as is the case for firms in the services sector. Age and ownership of the firm explain heterogeneity in inflation expectations (Chart 7, panel b).

Chart 7

Inflation expectations at different horizons and relationship between firm characteristics and inflation expectations

a) Inflation expectations

(annual percentages)

b) Firm characteristics and inflation expectations

(percentage points)

Sources: Survey on the Access to Finance of Enterprises.

Notes: Panel a) shows survey-weighted median firms’ expectations for euro area inflation in one year, three years’ and five years’ time. Panel b) shows the relationship between firm characteristics and one-year ahead inflation expectations. Robust standard errors are considered for the 95% confidence intervals.

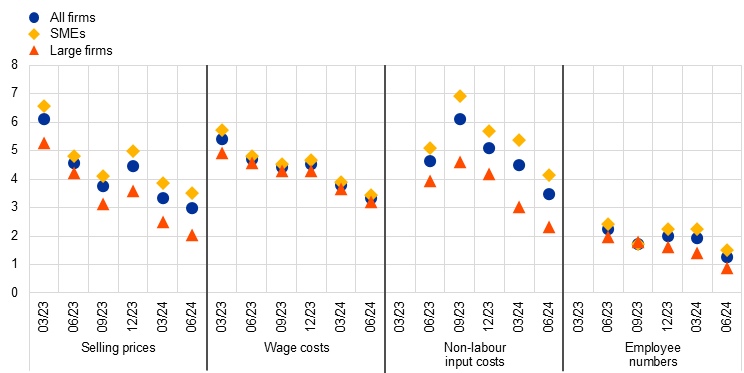

Since early 2023, the SAFE has also asked firms about their expected selling prices, wages, input costs and number of employees one-year ahead. Firms are asked in the survey to indicate the expected change over the next 12 months in: i) the average selling price of own products or services in their main markets; ii) the average price of production inputs (non-labour costs, such as materials and energy); iii) the average wage of current employees; and iv) the number of employees.

Growth rates in expected selling prices, wage costs and non-labour input costs have significantly slowed in recent periods (Chart 8, panel a). In March 2023, firms expected their selling prices to increase by 6.1%, on average, over the next 12 months, yet this percentage decreased to 3% by June 2024. Wage growth expectations declined from 5.4% to 3.3% over the same period. Throughout the entire period, SMEs consistently anticipated higher increases in both selling prices and non-labour input costs compared with large firms.

Higher expected wage costs tend to be correlated with higher expected selling prices, albeit this relationship has weakened slightly over the past year (Chart 8, panel b). A regression which analyses firms’ expected changes in non-labour input costs suggests that a 1 percentage point increase in wage expectations is, on average, associated with a 0.18 percentage point higher selling price expectation in June 2024. This relationship has become slightly weaker over the past four quarters. The results suggest that future declines in average wage cost expectations could translate into decreases in firms’ selling price expectations, albeit at a slower pace.

Chart 8

Firms’ expectations for selling prices, wages, input costs and employee numbers one-year ahead

a) Firms’ expectations by size

(percentage changes over the next 12 months)

b) Impact of changes in wage costs on selling prices

(percentage point change in expected selling price associated with a 1 percentage point expected change in wage costs)

Source: Survey on the Access to Finance of Enterprises.

Notes: SMEs stands for small and medium-sized enterprises. Panel a) shows average survey-weighted euro area firms’ expectations of changes in selling prices, wages of current employees, non-labour input costs and the number of employees for the next 12 months across size classes. The statistics are computed after trimming the data at the country-specific 1st and 99th percentiles. Panel b) shows the estimated coefficients of wage cost expectations from regressions, computed separately for each time period, of expected price changes on expected wage changes, controlling for expected changes in other input costs. Standard errors clustered by firm size sector and country.

6 Conclusions

Over the past 15 years, the SAFE has been an important source of data for assessing the access to finance of firms in the euro area. The survey has played an important role in understanding the transmission of monetary policy to firms’ financing conditions. Furthermore, the survey has shed light on how changes in financing conditions affect firms’ economic performance and their business cycles.

The recent increased frequency of the survey and the introduction of questions on firms’ euro area inflation expectations have made this survey even more valuable for the ECB’s monetary policy transmission assessment. Together with the introduction of questions on expectations of selling prices and input costs, the survey has closed a gap in the availability of such data for firms in the euro area.

This article covers the survey results from the third survey round, from April to September 2010, and until the 31st survey round, from April to June 2024.

The ECB collects information on inflation expectations from households through the Consumer Expectations Survey; from professional economists through the Survey of Professional Forecasters and from market participants through the Survey of Monetary Analysts.

See the box entitled “Climate change and euro area firms’ green investment and financing ‒ results from the SAFE”, Economic Bulletin, Issue 6, 2023, and the SAFE report for the second quarter of 2024.

For further details on the financing gap indicator introduced in 2013, see Ferrando, A. et al., “Measuring the opinion of firms on the supply and demand of external financing in the euro area”, IFC Bulletin, No 36, Bank for International Settlements, 2013, and Box 1 of this article.

Firms incur these market funding costs when raising capital through financial markets, such as by issuing bonds or equities.

For a detailed discussion of the ECB’s monetary policy decisions during these periods see Lane, P.R., “The 2021-2022 inflation surges and monetary policy in the euro areaThe ECB blog”, , 11 March 2024, and Rostagno, M., Altavilla, C., Carboni, G., Lemke, W., Motto, R., Saint Guilhem, A. and Yiangou, J., “Monetary Policy in Times of Crisis: A Tale of Two Decades of the European Central Bank”, Oxford University Press, 2021.

This phase incorporated the introduction of negative rates in June 2014, the start of the targeted longer-term refinancing operations (TLTRO I) in September 2014, the launch of TLTRO II and TLTRO III, together with the corporate sector purchase programme.

At the peak of the pandemic, the ECB announced widespread measures to support the functioning of credit markets, such as the recalibration of conditions for TLTRO III operations with highly accommodative conditions for banks, the expansion of the asset purchase programme and the start of the pandemic emergency purchase programme. European governments responded to the outbreak of the pandemic by deploying large fiscal packages. For further details of these packages, see the box entitled “The impact of fiscal support measures on the liquidity needs of firms during the pandemic”, Economic Bulletin, Issue 4, ECB, 2021.

See Euro area bank lending survey and the article entitled “Happy anniversary, BLS – 20 years of the euro area bank lending survey”, Economic Bulletin, Issue 7, ECB, 2023. Additionally, see Ferrando A., Holton, S. and Parle, C., “The transmission of bank credit conditions to firms – evidence from linked surveys”, Working Paper Series, No 2975, ECB, 2024, for insights on the impact of bank credit standards on firms’ access to finance.

The most recent wave of survey responses available for this article covers the second quarter of 2024 and was conducted between 28th May and 20th June. Therefore, the impact of the interest rate change in June 2024 cannot be fully assessed.

For seminal papers on the bank lending channel, see Bernanke B. and Blinder A., “Credit, Money and Aggregate demand”, The American Economic Review, Vol. 78, No 2, American Economic Association, May 1988, pp. 435-439, and Kashyap, A.K. and Stein, J.C., “The impact of monetary policy on bank balance sheets”, Carnegie-Rochester Conference Series on Public Policy, Vol. 42, Elsevier, June 1995, pp. 151-195.

See Ferrando, A., Popov, A. and Udell, G., “Unconventional monetary policy, funding expectations, and firm decisions”, European Economic Review, Vol.149, Elsevier, October 2022, pp.1-24.

See the box entitled “Firms’ access to finance and the business cycle: evidence from the SAFE”, Economic Bulletin, Issue 8, ECB, 2022.

See Ferrando, A. and Forti-Grazzini, C., “Monetary policy shocks and firms’ bank loan expectations”, Working Paper Series, No 2838, ECB, 2023.

See, for example, the box entitled “Substitution between debt security issuance and bank loans: evidence from the SAFE”, Economic Bulletin, Issue 1, ECB, 2023.

See also the article entitled “Assessing corporate vulnerabilities in the euro area”, Economic Bulletin, Issue 2, ECB, 2022.

See the box entitled “Firm’s access to finance and the business cycle: evidence from the SAFE”, Economic Bulletin, Issue 8, ECB, 2023.

See Baumann U. et al., “Inflation expectations and their role in Eurosystem forecasting”, Occasional Paper Series, No 264, ECB, September 2021.

See Baumann U., Ferrando, A., Georgarakos, D., Gorodnichenko, Y. and Reinelt, T., “SAFE to update inflation expectations? New survey evidence on euro area firms”, Working Paper Series, No 2949, ECB, 2024, for an analysis of the properties and causal effects of firms’ euro area inflation expectations.