- THE ECB BLOG

How banks deal with declining excess liquidity

18 June 2024

With the reduction of the Eurosystem’s balance sheet, central bank liquidity is declining. As liquidity is unevenly distributed among banks, an effective redistribution and use of market funding are essential. This worked well so far, with limited recourse to Eurosystem’s refinancing operations.

During and after the COVID-19 pandemic, the Eurosystem purchased large amounts of bonds and lent liquidity to banks at favourable interest rates. These measures ensured favourable financing conditions in support of the economic recovery and the achievement of the ECB’s price stability mandate when inflation was below-target. At the same time, the measures injected large amounts of liquidity into the banking sector much beyond banks’ required holdings of central bank liquidity. Therefore, excess liquidity[2] increased significantly, reaching a peak of EUR 4.7 tn in November 2022. Since then, the central bank balance sheet has been normalising and in turn excess liquidity has declined by 31% to EUR 3.2 tn until May 2024 (Chart 1).

Chart 1

Excess liquidity evolution and its drivers (EUR billions)

Source: ECB, ECB calculations.

Notes: The future paths of monetary policy portfolios and credit operations are based on the median expectations by analysts as reported in the latest SMA surveys. The projection of excess liquidity is based on these projections subtracting the projections of autonomous factors and minimum reserve requirements, based on ECB internal assumptions and models.

Excess liquidity is expected to remain ample for some time considering the gradual decline going forward (Chart 1). However, the experience of several crises, a changed regulatory environment and banks’ stricter risk management practises suggest that banks will want to hold on to more central bank liquidity as a buffer than before. Of course, the desired amount of extra reserves will differ across banks and will depend on their risk preferences or business model. Moreover, given that liquidity is unevenly distributed across banks, reflecting the diverse liquidity needs and business models across the euro area and banks, some may face liquidity shortages much earlier than others. That raises the question how banks are adjusting to an environment of lower aggregate liquidity and whether liquidity is flowing effectively from banks with still abundant liquidity to those with emerging liquidity needs. If such a redistribution was impaired and banks were at the same time reluctant to borrow from the ECB in its standard refinancing operations, this could give rise to liquidity shortages, volatility in money market rates and ultimately hamper the smooth transmission of monetary policy. Let’s take a look at two markets that are particularly important for the redistribution of liquidity among banks: the repo market and the covered bond market.

Is liquidity flowing effectively between banks?

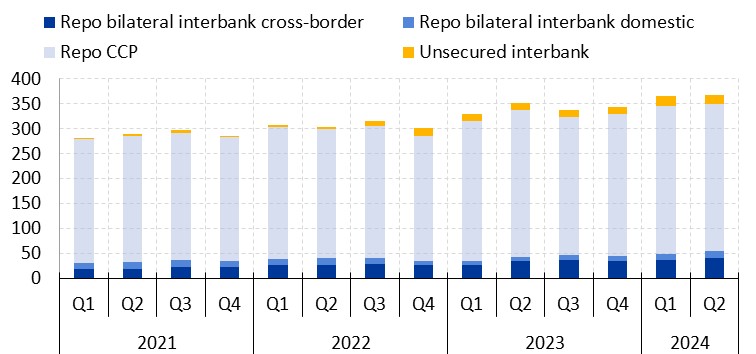

Repo markets[3] have been a crucial channel for effectively distributing liquidity among banks. In this highly liquid market banks lend and borrow cash against collateral among each other. With excess liquidity declining, banks have visibly increased their activity in repo - or so-called secured money markets - a sign of banks increasingly tapping this market for active liquidity management. Also the unsecured interbank market activity slightly increased but remains very limited in size, mainly due to its costs from a regulatory perspective, and concentrated among German banks (Chart 2).

Repo markets are also increasingly used to help fulfilling liquidity regulation requirements. The increase in repo volumes was mainly driven by transactions with maturities of 1-month and above, which are more valuable from a regulatory perspective compared to short-term maturities, and increasingly conducted against bank bonds, especially covered bonds, thereby transforming assets that are less liquid into the most liquid asset: cash held at the central bank.[4]

Zooming into repo activity indicates a well-functioning market. In fact, the higher volume in the repo market has gone hand in hand with more banks trading with each other across borders and little indications for more price dispersion in the market.

Chart 2

Borrowing volumes in the unsecured and secured money market with banks and central clearing counterparties (CCPs) (EUR billion)

Sources: ECB, MMSR, ECB calculations.

Notes: Chart displays secured (repo) volumes based on MMSR reporting agents borrowing cash from euro area banks or from CCPs against any collateral. The bilateral volumes are further split between the domicile of the trade counterparties highlighting the cross-country distribution. Transactions with centrally cleared counterparties (CCPs) do not allow to identify the location of the ultimate counterparty or its sector, therefore might capture also trades with non-banks. Unsecured interbank trades capture activity between euro area banks which remain limited. For more details about activity in the different euro area money market segments, please see the Euro money market study. Last observation: 16 May 2024.

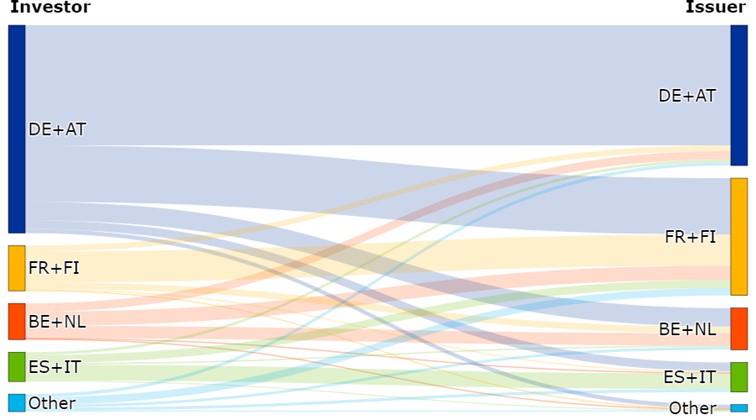

In addition, covered bonds have played a special role in the funding and liquidity redistribution in the euro area banking system. Ahead of the Targeted Longer-Term Refinancing Operations (TLTRO) repayments, banks increased their market-based funding, notably via the issuance of covered bonds. Covered bonds are secured bank debt securities that are collateralised with public sector debt or mortgage loans and where investors benefit from a double-recourse protection. Covered bonds, as other fixed income instruments, became particularly attractive for investors when yields moved higher since 2022. Interestingly, banks were a major investor absorbing a large part of the covered bond issuance of other banks.[5] As banks have invested in covered bonds of their peers, including in different jurisdictions, this has further contributed to redistributing liquidity within the euro area banking system (Chart 3).

Chart 3

Banks’ investments in covered bonds issued since the end 2021, split by jurisdictions (%)

Source: ECB, SHS.

Notes: The chart shows which jurisdictions purchased (LHS, investor) the covered bonds issued since the end of 2021 (RHS, issuer), by taking a snapshot view of banks’ holdings at the end of Q1 2024. The universe includes CBPP3 eligible covered bonds from Germany (DE), Austria (AT), France (FR), Finland (FI), Belgium (BE), Netherlands (NL), Spain (ES), Italy (IT) and all other euro area countries that issue covered bonds. The grouping of countries is based either on investors that have broadly similar geographical preferences, or where the proportion of investor/issuer is comparable.

How to read the figures: From left to right one can follow the flow of investments. For example, German and Austrian banks together seem to have played a larger role as investors then they have as issuers. Thus, while they invested significantly in their own domestic market, they have also played a relevant investor role in other jurisdictions, redistributing liquidity.

Do banks seek more liquidity via ECB’s standard refinancing operations?

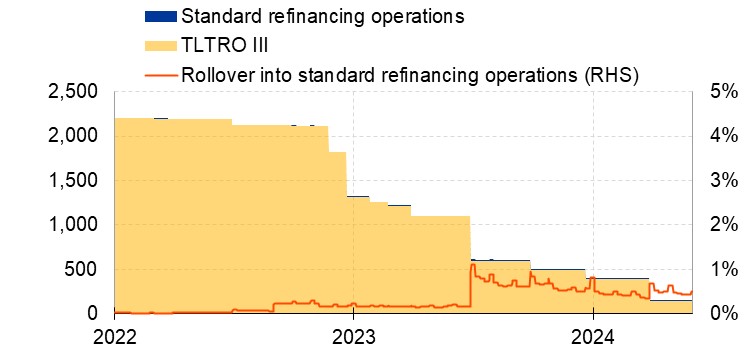

As excess liquidity remains high and the redistribution among banks via repo and covered bond markets is working well, there was only a limited increase in the usage of central bank refinancing operations until now. Without such high levels and smooth liquidity flows, one could have expected that some banks would be forced to make more use of the ECB’s standard refinancing operations, in particular, to replace the maturing TLTRO loans. That has, however, not been the case until now. Less than 1% of the peak of outstanding TLTROs was rolled over into standard refinancing operations, like the Main Refinancing Operation (MRO) or the 3-month Longer-term Refinancing Operation (LTRO) (Chart 4).

Chart 4E

volution of outstanding amounts of standard refinancing operations and TLTRO III (LHS: EUR billion, RHS: percentages)

Source: ECB (MOPDB) and ECB calculation.

How to read the figures: The shaded areas represent the outstanding amounts of TLTRO III (yellow), and MRO and 3-m LTRO (blue). The red line represents the share of standard refinancing operations (MRO and 3-M LTRO) compared to the peak of TLTRO III recourse as a proxy for the rollover from TLTRO III into standard refinancing operations.

Conclusion

The reduction of excess liquidity is progressing, which has triggered banks to tap market-based sources of funding. In this context secured funding instruments, such as repo and covered bond markets, have been important to support the redistribution of excess liquidity across the euro area banking system. More funding needs will emerge as excess liquidity declines further and excess liquidity remains unevenly distributed within and across countries. This will require further redistribution of liquidity at a larger scale than observed today. The recently announced changes to our operational framework aim to address the corresponding challenges, offering standard refinancing operations at fixed rate full allotment at a lower spread of 15 bps between the interest rate on the MRO and the deposit facility as of 18 September 2024. This narrower spread will incentivise bidding in the weekly operations, so that short-term money market rates are likely to evolve in the vicinity of the deposit facility rate and will therefore limit the potential scope for volatility in short-term money market rates. At the same time, it will leave room for money market activity and provide incentives for banks to seek market-based funding. As the reduction of excess liquidity progresses, the Eurosystem’s standard refinancing operations are intended to play a central role in meeting banks’ liquidity needs and their use by banks is an integral part of a smooth implementation of monetary policy.

The views expressed in each blog entry are those of the author(s) and do not necessarily represent the views of the European Central Bank and the Eurosystem.

We are grateful to Kristian Tötterman, Julian von Landesberger and Mihail Medvedi for their contribution to this blog post.

Excess liquidity refers to the amount of central bank reserves held by commercial banks over and above minimum reserve requirements.

Repo refers to repurchase transactions (short-term loan), where one party sells a financial asset with a simultaneous commitment to repurchase that asset at a future date. Repo is a form of secured cash lending against collateral and represents an important liquidity redistribution channel in the euro area.

When banks pledge financial assets defined by regulation as “non-high quality liquid assets” (non-HQLA) as collateral in a repo transaction, they can convert them into reserves (which are of the highest quality and liquidity), therefore improving their liquidity coverage ratio (LCR).

In the euro area banks traditionally held around 30% of publicly placed covered bond issuance. This share temporarily decreased while the Eurosystem increased its covered bond holdings through the CBPP3. Banks have now quickly recovered their market share by playing an overwhelming role as an investor from 2022 to early 2024, as they absorbed around 70% of net issuance of covered bonds. German bank treasuries historically show a particular preference for this type of securities.